Parliament Approves One-Year Extension for Due Diligence Rules and Two-Year Delay for Sustainability Reporting

The European Parliament has overwhelmingly voted to postpone the implementation of new EU laws requiring companies to meet due diligence and sustainability reporting requirements, marking a significant shift in the timeline for corporate compliance across the European Union.

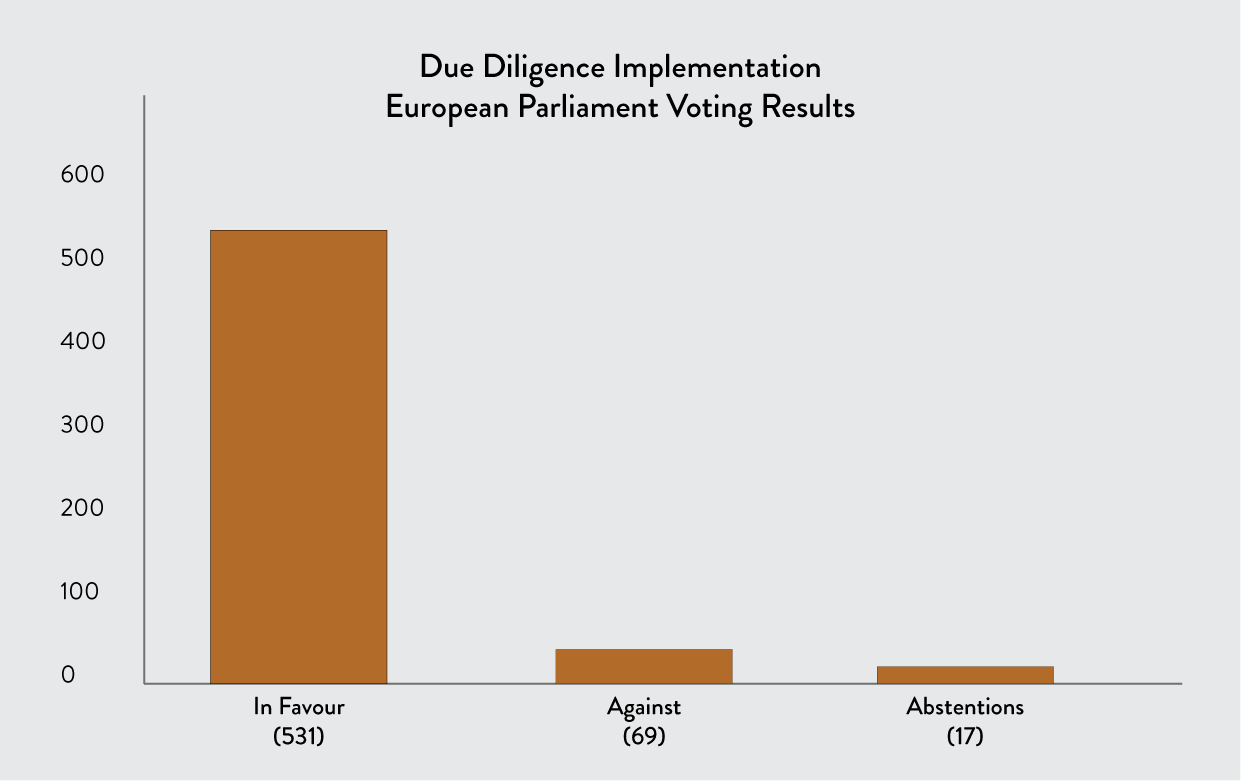

In Thursday’s session, MEPs voted 531 in favour, with 69 against and 17 abstentions, supporting the European Commission’s proposal to delay these regulations as part of broader efforts to enhance EU competitiveness through regulatory simplification.

Due Diligence Implementation Timeline Extended

The corporate due diligence rules, which require companies to identify and mitigate their negative impacts on human rights and the environment, will now follow a revised timeline:

- Member states will have until July 26, 2027 – an additional year beyond the original deadline – to transpose these requirements into national legislation

- The first wave of affected businesses will need to apply the rules from 2028, rather than 2027

- This first wave includes EU companies with over 5,000 employees and net turnover exceeding €1.5 billion, along with non-EU companies reaching this turnover threshold within the EU

- The second wave of companies – those with over 3,000 employees and net turnover above €900 million – will also begin compliance in 2028, maintaining the original staged approach but with the one-year delay

Sustainability Reporting Directive Also Delayed

The Corporate Sustainability Reporting Directive (CSRD) will also see significant postponements:

- Large companies with more than 250 employees will now be required to report on their social and environmental measures for the first time in 2028, covering the 2027 financial year

- Listed small and medium-sized enterprises will follow a year later, with first reporting in 2029

- This represents a two-year extension for both the second and third waves of companies covered by the legislation

Industry observers note that while the core requirements remain unchanged, the extended timeline provides businesses with additional preparation time amid current economic challenges.

Due Diligence Implementation Timeline Extended

The corporate due diligence rules, which require companies to identify and mitigate their negative impacts on human rights and the environment, will now follow a revised timeline:

- Member states will have until July 26, 2027 – an additional year beyond the original deadline – to transpose these requirements into national legislation

- The first wave of affected businesses will need to apply the rules from 2028, rather than 2027

- This first wave includes EU companies with over 5,000 employees and net turnover exceeding €1.5 billion, along with non-EU companies reaching this turnover threshold within the EU

- The second wave of companies – those with over 3,000 employees and net turnover above €900 million – will also begin compliance in 2028, maintaining the original staged approach but with the one-year delay

Sustainability Reporting Directive Also Delayed

The Corporate Sustainability Reporting Directive (CSRD) will also see significant postponements:

- Large companies with more than 250 employees will now be required to report on their social and environmental measures for the first time in 2028, covering the 2027 financial year

- Listed small and medium-sized enterprises will follow a year later, with first reporting in 2029

- This represents a two-year extension for both the second and third waves of companies covered by the legislation

Industry observers note that while the core requirements remain unchanged, the extended timeline provides businesses with additional preparation time amid current economic challenges.

Part of Broader Simplification Efforts

The delays form part of the Sustainability Omnibus initiativehttps://ec.europa.eu/commission/presscorner/detail/en/qanda_25_615

presented by the European Commission on February 26, 2025. Beyond timeline adjustments, the package includes substantive changes to the content and scope of sustainability reporting and due diligence requirements.

Work on these substantive modifications will now begin in the Parliament’s Legal Affairs Committee, with stakeholders watching closely to see how the requirements may be adjusted.

Rapid Legislative Process

To expedite the implementation of these changes, Parliament agreed to handle the file under its urgent procedure. The legislation now requires only formal approval from the Council of the European Union, which has already endorsed the same text on March 26, 2025.

Business groups have generally welcomed the postponement, arguing it provides needed breathing room to properly implement these complex requirements. Environmental and human rights organizations, however, have expressed concern that delays could slow progress toward more sustainable and ethical business practices across Europe.

The decision reflects the EU’s ongoing effort to balance ambitious sustainability goals with practical business considerations in a challenging economic climate.

Comment

The European Parliament voted to postpone the Corporate Due Diligence and Sustainability Reporting requirements to “allow more time for debate and consideration” of the proposed regulations. Concerns were raised regarding the impact of these requirements on businesses, particularly small and medium-sized enterprises, as well as the need for further clarification on certain aspects of the legislation.

Stakeholders in the context of Corporate Due Diligence and Sustainability Reporting typically include:

- Corporations: Companies that are subject to the regulations and must comply with reporting requirements.

- Investors and Shareholders: Individuals and institutions that invest in companies and are interested in their sustainability performance and risk management practices.

- Consumers: The general public who make purchasing decisions based on a company’s sustainability practices and corporate social responsibility.

- Employees: Workers within the organizations who may be affected by corporate policies and practices related to sustainability and ethical conduct.

- Regulatory Bodies: Governmental and intergovernmental organizations that establish and enforce legal requirements and standards for corporate conduct.

- Non-Governmental Organizations (NGOs): Advocacy groups that focus on environmental issues, human rights, and other aspects of corporate responsibility.

- Community Groups: Local organizations and residents who may be impacted by a company’s operations and sustainability practices.

- Academics and Researchers: Individuals studying corporate practices and their effects on society and the environment.

- Supply Chain Partners: Businesses that work with corporations and are influenced by their sustainability policies and practices.

These stakeholders each have different interests and perspectives regarding corporate responsibility, sustainability, and due diligence, making their involvement crucial in shaping effective regulations and practices. They have sought to ensure that the regulations would be effective in promoting sustainability and corporate responsibility without imposing undue burdens on companies. The postponement aimed to facilitate a more thorough discussion to balance regulatory goals with practical implementation.

The emphasis on granular data, accuracy in calculations, and transparency in communication will likely remain central to the revised Corporate Due Diligence and Sustainability Reporting requirements. As the goal of these regulations is to ensure that companies provide detailed, reliable information about their sustainability practices and potential impacts on human rights and the environment.

Granular data helps stakeholders, including investors and consumers, make informed decisions based on the sustainability performance of companies. Continued focus on accuracy and transparency is intended to build trust and accountability in corporate sustainability efforts.

As discussions progress, it will be important to monitor any updates or adjustments to the requirements to understand how they will evolve and what specific guidelines will be implemented.

Recent Comments